0:00 - Introduction

Other academic studies have explored the returns to value through the construction of zero-cost portfolios (i.e., buying value stocks while shorting growth stocks). These studies have shown significant excess returns to value that, depending on the study, have noted various risk-based and behavioral-based drivers.

In this paper called "Deep Value", by Cliff Asness and several of his colleagues at AQR Capital Management, the authors explore the returns to deep value portfolios (i.e., zero cost value portfolios occurring at times when the spread between value and growth company values are unusually large).

0:23 - Table 2. Summary Statistics and Value Performance

First, the authors provide some sample statistics and explain their methods for portfolio formation. In their study, their data includes price/return statistics for stocks in the US, Japan, Europe, and UK markets; and index futures for equities, fixed income and currencies. In the case of US equities, data goes back to 1926, and the other regions and asset classes generally begin in the 1970s and 1980s, ending in 2015.

For each of the asset classes and regions, the authors sort them by their Price-to-Book ratios (or the equivalent figure, in the case of non-equity asset classes) each month, and they put them into zero cost portfolios going long the top third of B/P ratios and going short the lowest third B/P ratios. The authors also sort by B/P ratios within intra-asset classes/regions (e.g., within industries; or by pairs for non-equity asset classes).

They find in all regions and asset classes (except UK equities), the zero-cost portfolios earn a positive sharpe ratio. These sharpe ratios are even more pronounced in intra-asset classes/regions.

5:28 - Table 3. Value Strategy Returns by Value Spread

Next, the authors organize the zero-cost portfolios into quintiles based on their "value spread" (i.e., the difference between the book-to-price ratios of the long portion of the portfolio vs the short portion of the portfolio). The thought is that when the value spread is larger (i.e., a "deep value" situation), we might see larger returns to value portfolios than time periods when the spread is narrower.

Indeed for all stock regions (except the UK) and asset classes, we do see increasing return as the value spread increases, monotonic increases for US equities. These are much more pronounced in the intra class portfolios. The non-equity asset classes exhibit the same results, albeit muted. When combining all stocks together, all non-equity asset-classes together, and all asset classes/regions together, we see monotonic increases in returns as the value spread increases. In addition, we see significant t-statistics for the top-ranked value spread portfolios, making these results robust.

10:57 - Table 4. Value Strategy Returns Regressed on Value Spreads

Next, the authors regress the returns of the zero-cost value portfolios (i.e., the dependent variable) against the value spread (i.e., the independent variable). They find the beta in the regression to be positive in all asset classes and regions, with significant t-statistics, giving evidence to the thought that returns to value are positively related to the value spread.

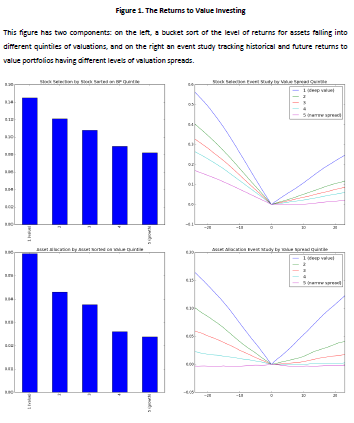

13:13 - Figure 1. The Returns to Value Investing

Next, the authors rank the stocks and non-equity asset classes by their book-to-price ratios and categorize them into quintiles based on those ranks. They find that as the level of book-to-price ratios decrease from high (i.e., value companies) to low (i.e., growth companies), the returns of those buckets decrease monotonically, which is in line with other studies who find that value companies tend to outperform growth companies on average.

Next, the authors perform an event study that shows cumulative returns of the zero-cost portfolio in the 24 months leading up to portfolio formation and up to 24 months after portfolio formation. They find that for all levels of value spread, the zero-cost portfolio has a negative return leading up to portfolio formation, then has positive returns up to 24 months after portfolio formation. This means that before portfolio formation, the value (i.e., long) side of the portfolio underperforms the growth (i.e., short) side; and after portfolio formation, the value (i.e., long) side outperforms the growth (i.e., short) side. These returns are more pronounced in deep value periods than in periods of a narrow value spread.

They performed the same analysis with non-equity asset classes (i.e., equity index, fixed income, and currency futures) as well, and find the same results.

17:36 - Figure 2. Risk Dynamics of Value Investing

Next, the authors perform the same analysis as with Figure 1, only this time they look at the market betas (rather than returns) for each B/P bucket. They find that the market betas are near 1 for each bucket, and they slightly decrease as the buckets move from value to growth.

They also perform an event study showing the market beta of the zero cost portfolio for 2 years before to 2 years after portfolio formation. They find that the betas (i.e., the beta of the long value side, minus the beta of the short growth side) are all below zero, signaling the zero-cost portfolio is a good hedge against market risk. We also see that periods of deep value result in even more significantly negative betas for the zero-cost portfolio, relative to the narrow value spread periods.

Next, the authors performed the same analysis, only this time they sort the quintiles by the value betas. As would be expected, the value portfolios load positively on the value factor and the growth portfolios load negatively on the value factor. Also, the zero-cost portfolio (i.e., going long value stocks and short growth stocks) tends to load more on the value factor during deep value periods than during narrow value periods. The zero-cost portfolio's loading on the value factor tends to decrease after portfolio formation as it becomes less "cheap".

The authors also perform the same analysis for non-equity asset classes and find the same results.

21:51 - Figure 3. Earnings Fundamentals of Value

Next, the authors perform the same analysis as in figures 1 and 2, but this time they present the return-on-equity for the different value vs growth buckets. Consistent with other research, they find the growth stocks tend to have larger returns-on-equity than do value stocks. They also perform an event study that shows the return-on-equity for the zero-cost value portfolio 24 months before and after formation. They find the returns-on-equity (i.e., the ROE for the long value, minus ROE for the short growth) decrease beginning 24 months before portfolio formation and continuing 24 months after portfolio formation, consistent with the idea that the ROE for growth companies exceed those of value companies. This decrease is also more pronounced during periods of deep value than for periods of narrow value spreads.

Next, the authors perform the same analysis, only this time they present analyst earnings revisions by bucket. They find that earnings revisions are negative for all buckets (as is consistent with the thought that analysts typically reduce earnings expectations rather than raise them); however, value companies tend to have the largest negative earnings revisions compared to growth companies. This is also evident in the event study which shows the earnings revisions of value minus the earnings revisions of growth stocks to decrease over time; this trend does seem to reverse a year after formation, however. Deep value events tend to exacerbate these results compared to narrow value spread events.

24:25 - Figure 4. News Sentiment of Value

Next, the same analysis as figures 1, 2, and 3 is performed, only this time the authors look at news sentiment across the different value/growth buckets and over the -2/+2 year event horizon. They find that growth companies tend to have more positive news sentiment than do value companies. During the 2 years leading up to the zero-cost value portfolio formation, the sentiment for growth stocks exceeds that of value stocks; however, in the 2 years after formation, the sentiment for value stocks exceeds that of growth stocks. Deeper value time periods show more extreme differences in sentiment between value and growth than do more narrow value spread periods.

26:02 - Figure 5. Demand Pressure

Next, the authors perform the same analysis as figures 1-4, only this time they look at demand pressure for value vs growth stocks (i.e., dollar buys, less dollar sells for stocks). They find that growth stocks tend to be more in demand than value companies. As a result of this, the cumulative difference between demand for the value side and the growth side of the demand pressure decreases over the 4 year event horizon; this difference tends to be more pronounced for deep value periods as opposed to narrow value spread time periods.

27:19 - Table 5. What Do Investors (Over-)React To

Next, the authors explore the drivers of the demand pressure and returns to zero-cost value portfolios, by regressing each of these against past returns and past return on equity.

They find the demand pressure is positively related to the past returns and past ROE; however, the ROE factor is subsumed by the past returns when combined in a regression. This signals that past returns and past ROE or correlated, and confirms prior studies that suggest investors over-extrapolate past returns when making investment decisions.

They also find the 1-month returns are positively related to 1-year past returns and negatively related to 5-year past returns, confirming prior studies that suggest investors over-react to past short-term returns, which results in initial momentum and a reversal later on. The authors also find that when controlling for past returns, the past ROE is positively related to the 1-month returns; this might suggest that investors under-react to fundamental information, consistent with other studies.

Next, the authors explore a few costs or hindrances to value arbitrageurs, which might be contributing to the persistence of value returns.

First, they find that bid-ask spreads for value companies tend to be much larger than those for growth companies. These bid-ask spreads for implementing the zero-cost value portfolio are more pronounced during deep value periods as opposed to narrow value spread periods.

Next, they find that short fees (i.e., the cost of shorting the growth side in the zero-cost portfolio) are expensive for both value and growth companies, but not so much for the interior buckets. Looking at the growth side only (because that's the side that is being shorted in the zero-cost portfolio), they find the short fees are much higher during periods of deep value as opposed to periods of narrow value spreads.

Finally, the authors find that value stocks tend to be more volatile than growth stocks. In addition, the volatility of the zero-cost portfolio is much higher during deep value periods compared to narrow value spread periods.

These higher bid-ask spreads, higher short fees, and higher volatility all present larger costs and risks to a value arbitrageur, therefore contributing to the persistence of excess value returns.

33:27 - Figure 7. Value Arbitrage Activity

Next, the authors explore whether investors (i.e., by shorting growth companies), the value companies themselves (i.e., through share buy-backs) or acquirers (i.e., by acquiring value companies) might be the value arbitrageurs.

First, they look at short-interest for the different buckets of value vs growth stocks. They find no meaningful difference between the short interest of growth companies than value companies. There is also not a meaningful change in short interest for growth companies over the 4 year event horizon; although, there is a dip around the portfolio formation time period possibly signaling investors' capital problems as growth stock prices are increasing as their short positions falter. There is much larger short interest for growth companies during deep value events as opposed to those of narrow value spread periods.

Next, the authors explore the difference in stock buy-backs for value vs growth companies, in an effort to determine whether the companies themselves are arbitraging their stock values that they perceive as cheap. They find that growth companies tend to issue more shares relative to value companies, although value companies still tend to issue more shares than they buy back. When exploring the buy-backs of the value companies minus the buy-backs of the growth companies, they find that after portfolio formation date, the value companies are buying back more shares than are the growth companies. This result is more pronounced for deep value periods compared to narrow value spread periods.

Finally, the authors explore whether acquirers are buying value companies when they get cheap. They find that value companies are acquired more often than are growth companies. They also find that the difference between the acquisition of value companies vs the acquisition of growth companies increases for the next two years after formation date; and this result is more pronounced for deep value periods compared to narrow spread periods.

All of this suggests that investors, the companies themselves, and acquirers are doing their part to arbitrage away the mispricing of value vs growth stocks; and these opportunities are taken advantage of more often when the value spreads get extremely deep.

37:21 - Table 6. The Alpha of Deep Value Out-of-Sample

Next, the authors explore out-of-sample tests for all 4 equity markets and all 3 asset classes to see what would the returns and characteristics of those returns have been under various trading strategies. First, they developed a trading strategy of buying into the zero-cost value portfolio (i.e., go long value companies and short growth companies) when the value spread (i.e., the spread between the B/P ratio of the value companies and the B/P ratio of the growth companies) exceeds its 80th percentile of data to that point; and exiting the zero-cost value portfolio when the value spread goes back below its median.

For each of the individual markets or asset classes, they find that the returns load significantly positively on the global value factor and significantly negatively on the momentum factor, with no significant loading on alpha (i.e., timing the value factor doesn't necessarily result in better performance than a passive value strategy). However, when all markets and asset classes are combined, they find a significant alpha figure.

The authors also perform this analysis for the intra-portfolios as well and find similar results, albeit with even more significant alphas.

39:51 - Table 7. The Alpha of Deep Value Out-of-Sample: Robustness

Next, the authors explore different trading strategies similar to the one in Table 6. They implement a "deep value" strategy (i.e., in at 80th percentile, out at median), "deeper value" strategy (i.e., in at 2 standard deviations, out at 1 standard deviation), "threshold" strategy (i.e., in at 80th percentile, out at 80th percentile), and "linear" strategy (i.e., allocation in proportion to the value spread level). They find that the "deeper value" strategy performs slightly better (i.e., it has a higher alpha) than the "deep value" strategy, and significantly better than the others; however, the results are similar across all strategies, where there are significant positive loadings to the value factor and alpha and a significant negative loading to the momentum factor. The intra-portfolios have similar results.

42:00 - Figure 8. Deep Value Strategy Cumulative Returns and Opportunity Set

Next the authors quantify and chart the cumulative returns to the "deep value" strategy as well as the opportunity set (i.e., the number of times the portfolios are in a "deep value" situation). They find deep value events clustered around significant world/US events, such as the 2001 and 2008 recessions, Iraq War in the early 90s, and Volker experiments. They also find significant and positive returns during the deep value event periods and across the entire sample period.

42:59 - Table 8. Deep Value Returns Vs The Number of Deep Value Opportunities

Finally, the authors developed a regression of returns, volatility, and sharpe ratios of the deep value portfolios against the size of the opportunity set. They find that the larger the opportunity set of deep value event periods, the higher the return, volatility, and sharpe ratios of the deep value strategy.

Abstract

We define “deep value” as episodes where the valuation spread between cheap and expensive securities is wide relative to its history. Examining deep value across global individual equities, equity index futures, currencies, and global bonds provides new evidence on competing theories for the value premium.Following these episodes, the value strategy has:

(1) high average returns;

(2) low market betas, but high betas to a global value factor;

(3) deteriorating fundamentals;

(4) negative news sentiment;

(5) selling pressure;

(6) increased limits to arbitrage; and

(7) increased arbitrage activity.

Lastly, we find that deep value episodes tend to cluster and a deep value trading strategy generates excess returns not explained by traditional risk factors.

Suggested Citation:

Asness, Cliff S. and Liew, John M. and Pedersen, Lasse Heje and Thapar, Ashwin K, Deep Value (December 1, 2017). Available at SSRN: https://ssrn.com/abstract=3076181 or http://dx.doi.org/10.2139/ssrn.3076181

Is there a crypto investment platform that obeys complete transparency and compliance? The actual reason why people like investing in cryptocurrency remains to make profit. OKGlobal operates with complete transparency, compliance, and comfort. It is a leading industry expert that stands as the future of investment and global currency management. OKGlobal is licensed, registered, insured, accredited and operates with the right regulatory authorities. The goal of this innovative digital asset platform is to ensure total safety and management for clients. https://www.okglobalcoinsg.com

ReplyDeleteNote : The first truly global STO that is open to the general public and has NO requirement to be an accredited or institutional investor.

#OKGlobalCoin #OkGlobalcoinswitch #Okglobal #securitytoken #smartcontract #blockchain #crypto #STO