The authors are going to examine the results of using three different methods of momentum for mutual fund portfolios over the period 1970 - 2004: ranking by past 6 month returns (JT), momentum factor loading (Beta4), and nearness to the 52-week high (52-week).

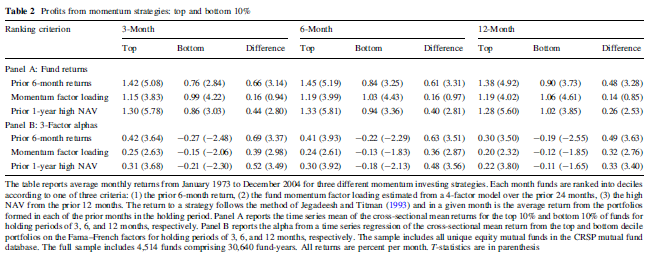

Table 2. Profits from momentum strategies: top and bottom 10%

The authors first rank the 3 methods using the top and bottom deciles, showing the long, short, and zero-cost returns. They find that the JT and 52-week strategies provide significant excess returns; however, the Beta4 strategy's excess returns are not statistically different than zero. The authors also analyzed these returns on a risk-basis, by putting the returns into the Fama-French 3-factor model and determining the alphas. They find all three strategies have significant alphas.

Table 3. Profits from momentum strategies: top and bottom 30%

Next, the authors perform the same analysis; but they rank the 3 methods with the top and bottom 30% of mutual funds (rather than the 10% in table 2). They find the same conclusion noted in table 2; although, the excess returns are a bit dampened now that the less extreme cases are included.

Figure 1. One-Month Raw Returns

Next, the authors summarize graphically the returns of the 10% zero-cost portfolio and the 30% zero-cost portfolio over a 12-month period for each of the three ranking strategies. It is clear that the JT and 52-week strategy have initial significant excess returns; however, those excess returns dissipate by the 12th month. The Beta4 strategy has initially low excess returns; but those returns are consistent throughout the 12 months and end the year with the highest of the three strategies.

Figure 2. One-Month Alphas

Next, the authors summarize graphically the alphas of the 10% zero-cost portfolio and the 30% zero-cost portfolio over a 12-month period for each of the three ranking strategies. Again we see the JT and 52-week strategy have initial significant excess returns; however, those excess returns dissipate by the 12th month, and the Beta4 strategy overtakes them.

Table 4. Comparison of momentum trading strategies

Next, the authors perform a Fama-MacBeth analysis of the three ranking strategies for the 10% and 30% zero-cost portfolios. They find the same results as tables 1 and 2; whereby the JT and 52-week strategies provide significant excess raw returns; however, the beta4 strategy lags. But all three strategies have statistically significant alphas over 3, 6, and 12 month time periods.

Figure 3. One-Month Hedged Alphas

Next, the authors take the results from table 4 and summarize them graphically over a 12 month period. As was found in the prior figures, we see the JT and 52-week strategy have initial significant excess returns; however, those excess returns dissipate by the 12th month, and the Beta4 strategy overtakes them.

Figure 4. Long-Term One-Month Alphas

Next, the authors decided to extend their period of analysis out to a 24-month holding period. They find that in the 13 to 24 month period, the JT and 52-week strategies continue to perform close to 0 hedged alphas, and the Beta4 strategy continues to outperform (although its hedged alpha slowly decreases over time). As such, a long-term investor might prefer using the Beta4 strategy to capture more consistent excess returns than the JT and 52-week strategies (whose excess returns seem to be short-term and fleeting.

Table 5-7. Comparison of momentum strategies: no-load funds

Next, the authors isolate the no-load funds within their population, as a way to explore whether the three strategies can be profitable on a practical trading basis. They explore the raw and risk-adjusted returns on the top/bottom deciles [Table 5], raw and risk-adjusted returns on the top/bottom 30% [Table 6], and hedged alphas on the top/bottom deciles and 30% [Table 7]. They find the same results as they found across all funds; therefore, these strategies could be implemented efficiently.

Table 8. Determinants of fund cash flows

Finally, the authors explore whether any of these three ranking strategies explain the cash flows into and out of a fund. They find that the JT and 52-week strategies significantly explain cash flows into a fund, but the Beta4 strategy does not. Other significant explanatory factors include total net assets, previous month's net cash flow, and expense ratio.

Sapp, T. (2011). The 52-week high, momentum, and predicting mutual fund returns. Review of Quantitative Finance & Accounting, 37(2), 149–179.

https://doi.org/10.1007/s11156-010-0199-7

George and Hwang (J Finance 59:2145-2176, ) have shown that the 52-week high share price carries significant predictive ability for individual stock returns, dominating other common momentum-based trading strategies. Based upon their results and other methods, this paper examines and compares the performance of three momentum trading strategies for mutual funds, including an analogous 1-year high measure for the net asset value of mutual fund shares. Strategies based on prior extreme returns and on fund exposure to stock return momentum are also examined. Results show that all three measures have significant, independent, predictive ability for fund returns. Further, each produces a distinctive pattern in momentum profits, whether measured in raw or risk-adjusted returns, with profits from momentum loading being the least transitory. Nearness to the 1-year high and recent extreme returns are significant predictors of fund monthly cash flows, whereas fund momentum loading is not.

No comments:

Post a Comment